Backtesting the GoldUxe Source Code V2.0 MQ4: A Masterclass in Validation

The search for a competitive edge in the volatile world of gold trading often leads to the discovery of specialized tools like the GoldUxe EA. For the savvy trader or developer, this search culminates in obtaining the "GoldUxe Source Code V2.0 MQ4" file—the very blueprint of the trading robot. Holding this source code feels like holding the key to a vault. But it is a key that has not yet been tested. The most critical and most frequently botched phase of using an Expert Advisor begins now: backtesting.

Anyone can run a quick test in MetaTrader 4 and produce a profitable-looking report. This is why most traders who use EAs fail. They mistake a simple backtest for true validation. This article is a masterclass designed to prevent that failure. Using the GoldUxe Source Code V2.0 as our live specimen, we will walk you through the professional-grade methodology for testing an EA. We will move beyond the misleading defaults, expose the trap of optimization, and teach you how to interpret the results like a quantitative analyst. This is how you transform a piece of code into a statistically validated trading strategy.

The Fatal Flaw of a Simple Backtest

Let's imagine you've opened the GoldUxe source code, compiled it, and launched MT4's Strategy Tester. You select the EA, choose XAUUSD, set the timeframe to M1, and hit "Start." Ten minutes later, you have a report showing a 300% profit. It's an exhilarating moment, and it is almost certainly a lie.

The default settings in the Strategy Tester are a recipe for disaster, especially for a high-frequency gold scalper like GoldUxe. Here’s why that first test is dangerously flawed:

- Modeling Quality: By default, MT4 may use the "Control Points" or even "Open Prices Only" model. This is woefully inaccurate. These models fabricate price data between candlesticks, completely missing the intra-bar price action where a scalper lives and dies. A scalping EA must be tested with the "Every Tick" model.

- The Spread: The tester uses a fixed, often unrealistically low spread (e.g., 2 pips). In the live market, the spread on Gold is variable and can widen dramatically during volatile periods, instantly turning a small winning trade into a loser.

- Ignored Trading Costs: The default test does not account for commissions, swaps, or slippage. Slippage—the difference between your expected price and the price at which the trade is executed—is a major factor in live scalping and a significant hidden cost that is ignored in a simple backtest.

Running a test under these perfect, artificial conditions doesn't validate the GoldUxe's strategy; it only proves it can be profitable in a fantasy world where trading is free and spreads are perfect.

Setting Up a Professional Testing Environment

To give the GoldUxe code a fair and honest trial, we must recreate the harsh conditions of the live market as closely as possible. This requires setting up a professional testing environment.

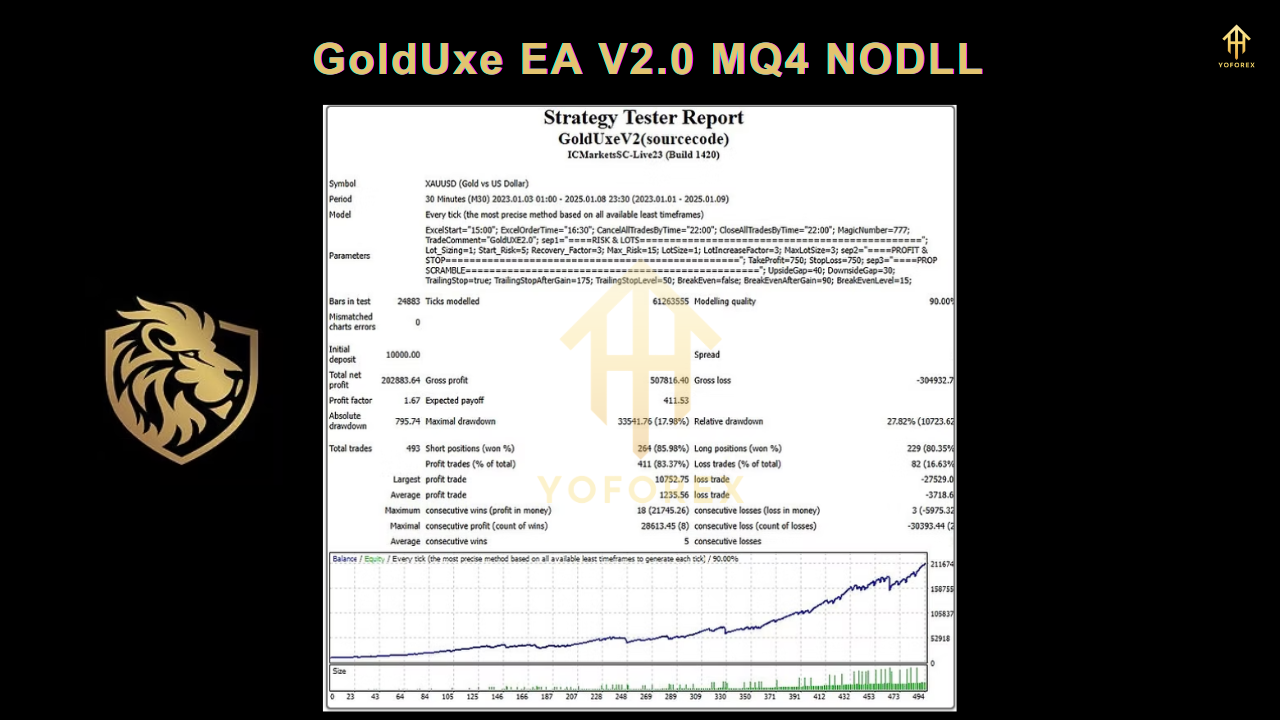

Acquire 99.9% Modeling Quality Tick Data: This is non-negotiable. Professional backtesting relies on historical data that includes every single real tick that occurred in the market. This is the only way to achieve 99.9% modeling quality, which is the industry standard for reliable testing. You cannot get this data from your broker or MT4 by default. You will need to use specialized software like Tick Data Suite or Tickstory to download and integrate high-quality, historical tick data into your MT4 platform.

Configure the Strategy Tester for Reality: Once you have quality data, you must configure the tester to use it. In the "Spread" setting, select "Variable" instead of a fixed value. This will use the real, historical spreads from your tick data. In your testing software (like Tick Data Suite), you can also enable simulation of slippage based on a set of parameters, which adds another layer of realism.

Match Your Broker's Conditions: Every broker is different. Go into the Strategy Tester's "Expert Properties." Under the "Testing" tab, set the initial deposit, leverage, and commission to match the live account you plan to use. A commission of $7 per round lot can have a massive impact on the profitability of a frequent scalper and must be included in your calculations.

The Peril of Optimization and Curve-Fitting

Now that the environment is set up, the temptation is to find the "best" settings for the GoldUxe EA. You open the "Inputs" tab, check the boxes next to parameters like TakeProfit, StopLoss, or MaxSpread, and run an "Optimization." The tester will now run hundreds of backtests to find the combination of inputs that produced the highest profit on your historical data.

This is the single biggest trap in automated trading. This process is called curve-fitting. You are not discovering a robust trading strategy; you are simply finding the exact parameters that were perfect for the past. These "perfect" settings have zero predictive power and will almost certainly fail as soon as they encounter new market conditions. The beautiful, optimized equity curve you created is an illusion. You have built a perfect key for a lock that no longer exists. A trader who takes these optimized settings and puts them on a live account is driving by looking only in the rearview mirror.

A More Robust Approach: Walk-Forward Analysis

So how do we test the parameters of the GoldUxe EA without curve-fitting? The professional solution is Walk-Forward Analysis (WFA). It is a much more robust and realistic testing methodology that simulates how a trader would actually use an EA over time.

Here's how it works in simple terms:

Define Periods: You divide your historical data into chunks. For example, if you have five years of data, you can create five "IN-SAMPLE" periods (each one year long) and five "OUT-OF-SAMPLE" periods (each three months long that immediately follow the in-sample period).

Optimize In-Sample: You run an optimization to find the best settings for the GoldUxe EA, but only on the first In-Sample period (Year 1).

Test Out-of-Sample: You then take those "best" settings from Year 1 and run a single backtest on the first Out-of-Sample period (the first three months of Year 2), without any further optimization. This tests if the settings are robust enough to work on unseen data.

Repeat the Process: You then move to the next chunk of data, optimizing on Year 2 and testing on the subsequent three months. You repeat this process for the entire data set.

The final Walk-Forward Analysis report combines all the Out-of-Sample periods. If the resulting equity curve is still positive and the drawdown is acceptable, it provides a much higher degree of confidence that the GoldUxe's strategy is truly robust and not just a product of curve-fitting.

Reading the Report: Beyond the Bottom Line

Whether you run a single robust backtest or a full walk-forward analysis, you must analyze the final report like a professional. Do not just look at the "Total Net Profit." That is a vanity metric. Focus on these key indicators of health:

- Maximal Drawdown: What was the largest peak-to-trough percentage loss? This is the best measure of the real risk you would have experienced.

- Profit Factor: The gross profit divided by the gross loss. A value above 1.5 is generally considered good; above 2.0 is excellent. A value near 1.0 means you are risking a lot for very little reward.

- Sharpe Ratio: This measures your return relative to your risk. A higher Sharpe Ratio is better.

- Total Trades: For a scalper like GoldUxe, you need a large number of trades (hundreds or thousands) for the results to be statistically significant.

Conclusion: A Verdict Born from Data

Having the GoldUxe Source Code V2.0 MQ4 is an opportunity, but it is not an answer. It is the beginning of a process of intense, data-driven scrutiny. The purpose of the rigorous backtesting methodology outlined in this masterclass is not to find settings that produce the most beautiful possible equity curve. The purpose is to understand the truth.

The goal is to discover the EA's true, unvarnished risk profile. It is to find its breaking points. It is to determine, with a high degree of statistical confidence, whether the "alpha" within its code is real and robust, or just a fleeting illusion created by over-optimization. A professional trader does not hope an EA will work; they test it until they know, with data, precisely how and when it is likely to fail. Only then can they make an informed decision about whether to risk their capital. By adopting this mindset, you transform yourself from a hopeful user into a quantitative analyst, and that is the most powerful edge of all.

Comments

Leave a Comment